Now is the time to strengthen our tourism infrastructure

Amidst the rubble and confusion from Covid 19, with international tourists restricted by airline operations and limited routes, country entry restrictions, and quarantine requirements and country limitations on social distancing, gatherings, and events, Jerusalem’s tourism sector is a mess. Already facing thin operating margins, hotels, restaurants, and bars are seeing mounting losses. Tour operators and guides are nearing financial collapse. And our world-class destinations, including museums, historic, and heritage sites are facing closures with operating losses – and no visitors. Let’s not waste this crisis.

We can take this opportunity to rethink our tourism sector by designing and implementing a tourism improvement district. A tourism district will allow Jerusalem to build financial and program mechanisms based on the collective strength of the Jerusalem region, not just individual tourism assets and destinations. It will allow us to create a competitive whole bigger than the sum of its parts. It will link biblical and recreational trails with destinations to tell compelling stories, attracting tourists to hear, see, learn and experience. The Kidron river valley is a good example of such a cluster of tourism assets, linking the soon to be clean river valley with monasteries, schools, farmers into a biblical, ecological, hiking, and environmental experience for international and Israeli tourists alike.

Such a tourism district will require money. And so we propose that now, when we have so little, is the time to design a hotel and hospitality tax for international tourists. Such a tax would allow for new revenues to the city and to support the development of the tourism infrastructure needed, including capital costs and operating costs to market these assets. This idea came up in our Financial Innovations Labs about financing heritage and archeological assets, and we have estimated the contours of two new taxes as part of a Financial Innovation Lab about Jerusalem and its fiscal condition in 2018 and updated to reflect the current Covid 19 world.

Jerusalem Institute for Policy Research, Milken Innovation Center estimate

Tourism tax

Tourism is a key industry in Israel, and especially in the Jerusalem region. Jerusalem is a key destination to international tourists in search of heritage and cultural attractions. Indeed, unlike other destination in Israel which are recreation-based (such as hiking and the beach), Jerusalem is unique historically, culturally, and religiously and therefore the demand by tourists does not respond to price. In a 2017 review of the tourism sector, we found that this lack of price sensitivity is common in major cultural tourist destinations in the world, such as London, Paris, Rome, and New York. It is in these areas, as it could be in Jerusalem, that the local governments may charge a tourism tax.

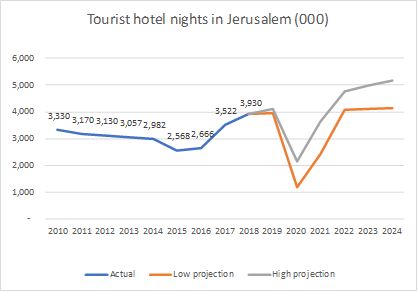

International tourism in Jerusalem reached a high point in 2019 with almost 1.2 million overnight tourists generating almost 4 million hotel room nights, and was expected to continue rising through 2020. A substantial loss in tourism is expected in 2020 with the Covid 19 pandemic, and a gradual rise beginning in 2021 and a return to prior levels in 2022.

A tourism tax may take many forms, including a bed tax, a service charge based on expenditure, a taxi and car rental tax, and a hotel room tax, but we recommending a hotel room tax on a nightly basis for international travelers. A room tax is a relatively small share of the cost of a stay in a hotel, is like the program in many other destinations in Europe and elsewhere, and is collected through a few, large establishments (hotels).

The steps to implement a hotel tax include:

- Through national enabling legislation and local statute, establish a per night, flat hotel tax for international visitors to be collected by the hotels.

- Establish a separate real estate tax rate for hotel ballroom and meeting room space (comparable to restaurant tax rate) to provide offset to hotels.

- Create an enterprise fund to collect per night hotel tax.

- Convene hotel industry committee to prioritize expenditures of tourism portion of budget.

- Distribute portion of new revenues to Municipality for operating expenses.

Many destination cities in the world have implemented hotel taxes. Two examples include Ashville, North Carolina which is a unique mountain destination with cultural, crafts, and unique music festivals. The hotel tax not only pays for tourism promotion, but it also supports financing for a range of infrastructures in the region. Rome is another example of a unique destination that charges a hotel tax. It has the highest hotel tax among EU destinations, and it is an important sources of revenues for the city’s budget.

In Jerusalem, with a NIS 30 per night hotel tax for international tourists, which is comparable with European hotel tax rates, and with expected collection losses, we estimate approximately NIS 47 million in new revenues to the Tourism Promotion Agency annually by year 10. In addition, we estimate approximately NIS 111.6 million annually in new revenues operations to the Municipality by year 10.

The new tax will:

- Create new source of capital to support tourism activities. The concept of a hotel tax has support in the tourism sector, especially if the implementation of the tax generates a new, sustainable source of revenue to support regional tourism.

- Tax from international tourists who are exempt from VAT and willing to pay. International travelers in Israel are exempt from paying the value-added tax (VAT), so they are already paying 17 percent less than Israeli tourists.

- Represent a small portion of the total cost of the hotel room expense.

- Allow the separation of large meeting areas from hotel real estate taxes equalizes tax burden on hotels, and the new taxes compensate for the lost revenues.

The risks from a hotel tax include:

- The ability to collect the hotel tax.

- Adds to the “cost” of a visit to Jerusalem if it is not implemented regionally or nationally.

- The global health crisis may restructure the global tourism patterns for years, so expectations of revenues may be difficult to predict.

- The enabling legislation would permit other local and regional authorities to implement a similar tax, which could increase the costs of tourism in those areas which may not be insensitive to price.

Source: AirDNA, AirBNB, and Milken Innovation Center estimates

Hospitality tax

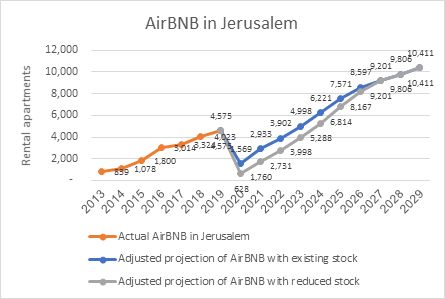

Short-term rental apartments have been a growing feature of the housing stock in the country. Starting as “holiday” apartment, international owners would rent apartments for stays during the summer and during the spring and fall holidays. This has left some apartment areas, especially close to tourist destinations like the Old City, like “ghost” villages during much of the year. The rise in short-term rental management companies has led to many of these apartments being filled with international tourists, especially with the rise in tourism over the last decade.

This trend has taken off like a rocket with AirBNB, allowing many owners to convert their apartments into profitable investments. Conversions of these apartments has been fast.[1]

Based on experiences in other cities both in Israel and internationally, we propose a new local tax on these short-term rentals. Specifically, we propose a hospitality tax on revenues from the use of a private home for rentals of less than one year (short-term rentals).[2] Following are the steps to implement this program:

- Establish a registry of hospitality facilities, homes available for short-term hospitality rental.

- Enact national enabling legislation to permit a tax on short-term rentals and enact a local statute to implement the program.

- Establish a hospitality tax based on a flat, per night rate for all visitors to AirBnB and other short-term rentals to be collected by the owner or manager of the short-term rentals.

- Create an enterprise fund (separate account for collection and distribution) for all proceeds from hospitality tax.

- Distribute portion of new revenues to Municipality for operating support.

With the proposed tourism tax on a nightly basis proposed above, and the need to ensure a level playing field with full hotels in the city, the annual new revenues from the tourism tax from nightly stays in short-term rentals such as AirBNBs would yield at additional NIS 25.7 million in new revenues.

The use of a tax on short-term rentals is in use in many areas already. AirBNB has facilitated over 400 agreements with local, state, territorial and national governments around the world to streamline and facilitate tax collection for hosts, most of whom are sharing their homes for extra income and may not be equipped for complex accounting processes. Voluntary Tax Collection agreements are in place in jurisdictions in the US, Canada, Latin America and Europe. Other examples include:

- Three French cities received tourist tax from Airbnb in 2019 are Paris (EUR 15.3M), Marseille (EUR 2.3M) and Nice (EUR 1.8M).

- Rome AirBNB hosts collect Euro 3.50 per person per night in a city lodging tax.

- In the US, Airbnb collects tourist taxes on behalf of hosts in thousands of jurisdictions. In practical terms, 72 percent of bookings made for Airbnb listings in the US are already covered by collection and remittance of tourism or hotel taxes.

The use of a hospitality tax puts the short-term market on an equal footing with hotels. In addition to generating new revenues from a new source, it brings revenues from outside the city. However, it will lead to increased costs for handling/reporting by the hosts, and complications and costs for accounting and management. With these complications, it may lead to a reduction in the conversions/offerings of short-term rentals through companies such as AirBNB or the increase in new services (and fees to the service provider) to short-term rental owners to handle this additional work. With the additional costs imposed on short-term rentals, it may lead to visitors arranging their overnight stays outside of the city, but this should be minimal given the desire to be within walking distance of destinations and services within a fully integrated tourism district.

Leveraging Future Revenues

Jerusalem can capture the future cash flows value created by these new revenues to invest in improving its tourism assets, paying operating expenses for promotion, and offsetting operating costs for the city and others.

Based on best practices from developed countries, the Milken Innovation Center recommends establishing a tourism development agency for Jerusalem to encourage economic growth, create jobs, and improve the quality of life for Jerusalem residents and visitors. Such an agency would be responsible for promoting Jerusalem as a tourist destination for Israelis and international visitors.

The agency could be incorporated as an independent public-private partnership between the tourism industry, community representatives, the Jerusalem Development Authority, and the Jerusalem Municipality. An independent agency that operates in partnership with the tourism industry will ensure stability of Jerusalem’s tourism promotion efforts.

Some might argue that NOW is not the time to impose economic costs on a weakened sector. With the acute losses in the sector, felt so sharply and broadly by all segments of the tourism sector, will it impede the rise in the sector? Will it slow the rise in tourists returning to Jerusalem? In economic, historic, and cultural terms, Jerusalem is unique in the world. To paraphrase the Prophets from the region, it will rebuild its tourism base. International tourism will return. Indeed, now is the exactly the time.

[1] The fall in apartments in 2020 results from the Covid-19 pandemic. With the dramatic drop in tourists and the high cost of carrying vacant apartments, AirBNB is seeing many owners converting apartments back to long-term rentals. This graph shows the drop in rentals, and the “permanent” loss of short-term rental stock, with a slow recovery over the next 5 years.

[2] Parenthetically, based on a breakdown among the apartments according to AirDNA, which analyzes AirBNB data globally, we estimated the average size (square meters) of the short-term rentals. Using the difference in the Arnona (real estate tax) rental rates for hotels and boarding establishments of less than 2000 square meters and the residential Arnona rate, we calculated the incremental Arnona which averages about 7 percent of the owner’s gross income from the short-term rentals. The estimated net new Arnona from short-term rentals is estimated at NIS 19.3 million per year by year 10.